"We make retirement easy, insightful and even a bit of fun. Get in touch today and find out how we help you make choices to make your retirement simple and effective."

Making the right choices within a (collective) pension contract can be complex. With the introduction of the Future Pensions Act, employees will have more freedom of choice and responsibility. This offers opportunities, but can also create uncertainty. PensionTime offers complete guidance so that employers and employees make the right pension decisions.

A good retirement and solid financial planning are key to a worry-free future. Whether you are at the beginning of your career or already closer to retirement age, it is never too early (or too late) to think about your financial future.

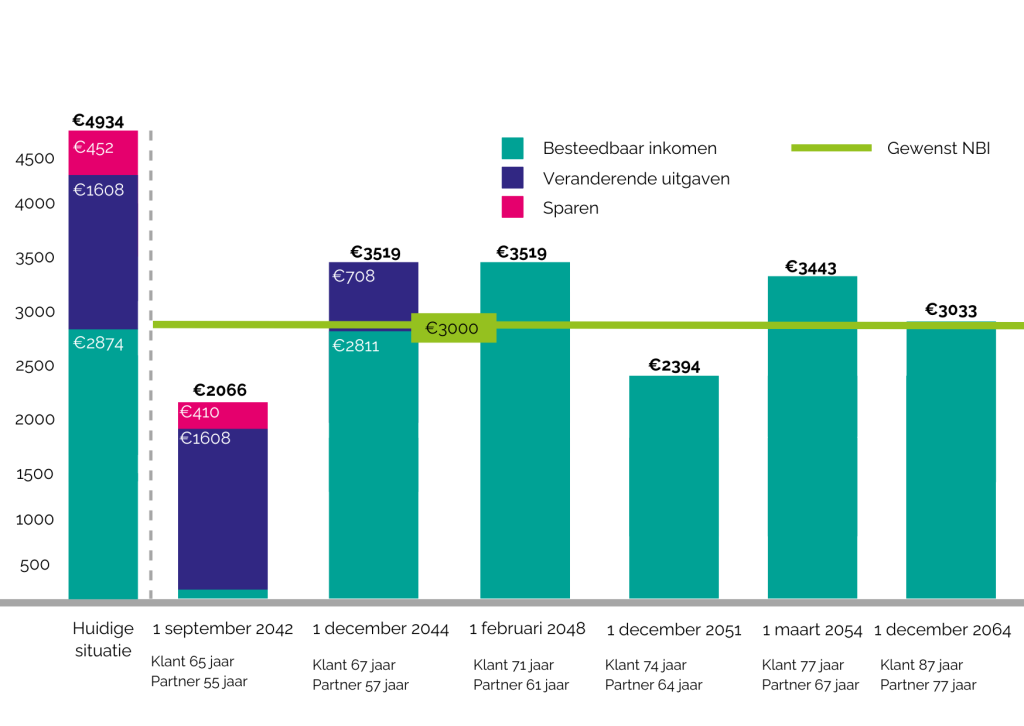

When a pension or annuity expires (lapses), there comes an important moment: you have to make decisions about what you want to do with this money. This could be a lifelong income or a payment over a certain period of time. But what are your options when your pension or annuity expires? And what choices do you have?

Just as your car needs a regular MOT inspection to make sure everything is working properly and you are safe on the road, the same applies to your pension. A Pension MOT is a check-up of your pension scheme to see if everything is still up-to-date and suits your needs and situation. The pension landscape is constantly changing due to new laws, such as the Future Pensions Act, and personal situations may also change, such as changes in work, income or family situation.

Choice guidance

Making the choices that suit youMaking the right choices within a (collective) pension contract can be complex. With the introduction of the Future Pensions Act, employees will have more freedom of choice and responsibility. This offers opportunities, but can also create uncertainty. Below are some of the choices available.

High-low, low-high

With a high-low construction, a worker can choose to receive a higher pension benefit first after retirement, followed by a lower benefit later. This can be beneficial, for example, if someone expects to incur more expenses in the first few years of retirement, such as travel.

A low-high construction is also possible, for instance if you expect healthcare costs to increase towards the future.

Earlier or later retirement

Employees can choose to stop working earlier or retire later.

Exchanging pension forms

Employees can choose to exchange a retirement pension for a partner's pension or vice versa. This can be important if, for example, someone does not have a partner or just wants extra security for the surviving partner.

Investment choices and reinvestment

Choosing between different investment profiles during the accumulation phase or choosing between guaranteed or variable benefits in the benefit phase is an important decision.

A guaranteed benefit offers security, but a variable benefit can yield more in the long run by continuing to invest. With the new rules, employees can in some cases continue to invest even after their retirement date to further grow their assets. We help choose the right investment strategy based on risk profile and financial goals.

Lump sum payment of 10%

From probably 2026, pensioners can choose to withdraw a one-off lump sum of up to 10% of their pension assets. This offers additional flexibility, for example to pay off a mortgage or make a major purchase. PensioenTijd helps weigh up the benefits and risks of this lump sum.

Choose PensioenTijd for expert choice guidance and ensure yourself an optimal pension plan that suits your wants and needs.

Pension planning

Towards a worry-free futureA good retirement and solid financial planning are key to a worry-free future. Whether you are at the beginning of your career or already closer to retirement age, it is never too early (or too late) to think about your financial future.

Retirement planning is not just about building up retirement money, but also about mapping out all your income, expenses, assets and debts. This way, you can ensure that you can live comfortably after retirement. Good financial planning helps you make smart long-term choices, such as paying off debts, investing in your future and building up a buffer.

Whether you are self-employed or salaried, smart retirement and financial planning will ensure that there are no surprises. By planning well now, you avoid financial worries later. PensioenTijd helps you draw up a tailor-made personal plan so that you are always well prepared, no matter what life brings.

Start your retirement planning today and ensure yourself a stable financial future!

Payout

What choices do you have?When a pension or annuity expires (lapses), there comes an important moment: you have to make decisions about what you want to do with this money. This could be a lifelong income, or a payment over a certain period of time. But what are your options when a pension or annuity expires?

What is an expiring pension or annuity?

An expiring pension or annuity means that the accumulation phase of your pension or annuity has come to an end. The accumulated capital is released, and now you have to choose how you want it to be paid out.

Choices for expiring pensions and annuities

When your pension or annuity expires, you have several options for how you want to receive the benefit. Here are some of the most common choices:

Lifetime benefit

A lifetime annuity means you receive a fixed amount every month until you die. This offers security because you will never run out of income, no matter how old you get. This is often a safe choice for those who value a stable, fixed income.

Temporary allowance

You can also opt for a temporary annuity where you have the money paid out over a shorter period, say 5, 10 or 20 years. In this case, the monthly payment will be higher than with a lifetime annuity, but the risk is that you will run out of income when the payout period is over.

Get paid immediately

Some people choose to have part of the accumulated capital paid out immediately. However, keep in mind that this is often subject to tax. This can be attractive if you want to make a large expenditure, but it can also have disadvantages because of the higher tax burden.

Bank savings

Another option is bank savings. Here, you leave the accumulated capital in a blocked savings account, where you can withdraw money periodically. This can be fiscally advantageous as you often pay less tax on these payments.

Pension and annuity shopping

It is possible to shop around with accrued pension capital and or accrued annuities at various providers. In short, we will see which provider will give you the best benefit for your accrued capital.

What should you pay attention to?

When making your choice, there are some important factors to consider:

Tax: Pay close attention to the tax rules. Some benefits are taxed higher than others.

Life expectancy: A lifetime allowance can be advantageous if you think you will reach an old age.

Financial targets: What are your financial needs and goals? Do you want a long-term fixed income, or do you prefer flexibility?

It is wise to seek financial advice before making a choice. PensionTime can help you choose the best option based on your personal situation. This way you avoid any surprises, and make sure you get the most out of your accrued pension or annuity.

Pension MOT

Keep your pension in top condition, just like your carJust as your car needs a regular MOT inspection to make sure everything is working properly and you are safe on the road, the same applies to your pension. A Pension MOT is a check-up of your pension scheme to see if everything is still up-to-date and suits your needs and situation. The pension landscape is constantly changing due to new laws, such as the Future Pensions Act, and personal situations may also change, such as changes in work, income or family situation.

During a Pension MOT, we check, among other things:

The pension to be achieved: Is your pension accrual still sufficient for your desired lifestyle after retirement.

Legal requirements: Does the current scheme still meet the legal requirements and adjustments, such as those from the Future Pensions Act.

Pension forms: Do the insured pension forms fit well with your situation, such as old-age, survivor and disability pension.

The choices made: Do the choices made around investing or guaranteed benefits still match your risk profile.

Personal changes: Is the pension scheme also adjusted to changes in your personal life, such as marriage, children, divorce or a new job.

Choose Pension MOT from PensioenTijd and make sure your pension scheme is ready for the future, just like you make sure your car stays safe to drive. Get started today and avoid problems later!